Securing a mortgage nowadays presents more challenges compared to two decades ago. During my tenure in the banking industry, a loan could easily be approved with just a photocopy of an identity card and salary vouchers. However, in today’s landscape, a more comprehensive set of documents and detailed borrower reports are required. We must acknowledge that we now live in a world of enhanced technology.

Twenty years ago, when borrowers approached us for loans, we primarily checked their CTOS records for bankruptcy. If they passed this check, I would submit the loan for approval. However, today, the CTOS system has evolved, incorporating many other borrower details. It’s astonishing that, in most cases, the system possesses more information about individuals than they do themselves.

Today, I’ll discuss the CTOS report. Another platform providing similar reports is called CCRIS, which we’ll cover in upcoming articles.

What is CTOS?

In simple terms, your CTOS report serves as your financial health assessment, aiding loan providers in evaluating your eligibility for borrowing.

Whether you like it or not, when you apply for a loan, banks will scrutinize your financial health. Instead of leaving this research solely to the banks, why not check your CTOS report yourself beforehand? This way, you’ll be better prepared when submitting a loan application and won’t be caught off guard.

There are two types of CTOS reports: a free version and a paid one.

The free report offers basic information, while the paid report, costing RM27.00, provides more comprehensive and useful details for borrowers. For our discussion, we’ll focus on the full report.

What’s included in the report?

- Personal Information

- Directorship & Business Interest

- Litigation & Bankruptcy

- Trade References

- CTOS Score

- CCRIS Record

- Dishonoured Cheques

For today’s discussion, we’ll delve into sections 2, 3, 5, and 6.

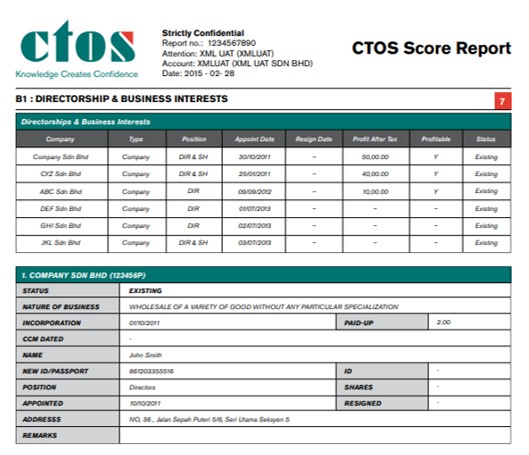

Directorship & Business Interest

This section lists any companies associated with the individual. Banks use this information to determine the number of companies an individual is involved with. Sometimes, individuals may disclose only one company, but upon checking, banks may find out about several undisclosed companies. If banks require unbiased information on these companies, they can conduct a CTOS search on them. As mentioned earlier, banks often know more about individuals than individuals do about themselves.

CTOS Score

What is it, and how does it work? These are common questions you may have.

The CTOS score determines your creditworthiness for the loan you’re applying for, indicating the likelihood of defaulting on repayments. Scores range from 300 to 850. If a borrower falls below the “fair” range, loan approval becomes more challenging. Banks become concerned about the higher risk associated with granting such loans. If borrowers discover that their score is below “fair,” it’s prudent to reassess their financial situation.

You might wonder what factors influence the score. They include:

a) Payment History (45%)

b) Amount Owed (20%)

c) Length of Credit History (7%)

d) Credit Mix (14%)

e) New Credit (14%)

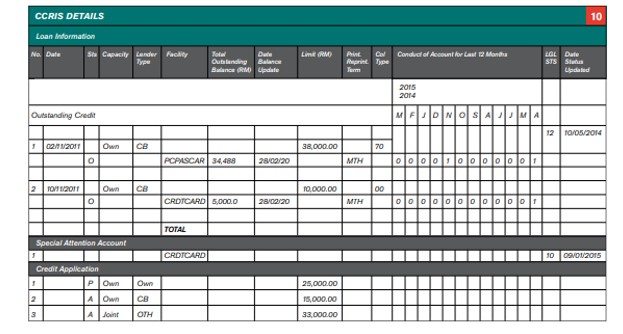

CCRIS Record

The Central Credit Reference Information System (CCRIS) is established by Bank Negara Malaysia’s Credit Bureau, offering standardized credit reports on prospective borrowers.

CCRIS acts as a centralized database, providing insights into your financial status. Monthly updates from relevant institutions furnish essential data such as banks, insurance providers, and government agencies. This process enables financial institutions to evaluate borrowers’ creditworthiness effectively by referencing their financial history records.

This section offers a detailed breakdown of each facility, including:

- Status of the facility

- Capacity

- Lender Type

- Facility Type

- Total Outstanding Balance

- Limit/Monthly Repayment

- Repayment Term

- Collateral Type

- Conduct of Account

- Legal Status

- Special Attention Account

- Credit Application Details

If the conduct of the account consistently shows a number higher than zero, say 3, it indicates the borrower is in a three-month default. Banks use this information to assess the likelihood of future defaults.

That’s a detailed overview of CTOS. I hope you find it helpful. Stay tuned for my next write-up, and don’t forget to subscribe.

From the desk of Michael Yeoh

Leave a comment