“The salesman smiled. You smiled. The bank smiled. The only thing not smiling was your wallet.”

Many Malaysians can tell you the interest rate of their car loan.

“Mine is only 2.8%.”

“Mine is 3%.”

Sounds cheap, right?

But what if I told you that for decades, many Malaysians have been paying much more interest than they realised — even when the loan agreement proudly displayed a seemingly low interest rate? The good news is that starting 1 June 2026, the rules are changing, and for once, consumers may finally get a fairer deal.

As someone who spends a lot of time talking about wealth building, property investment, and financial freedom, I believe this is one of the most important financial changes Malaysians should understand this year.

Because whether you are buying a Myvi, a Hilux, a Tesla, or a luxury continental car, your loan could impact your ability to buy a house, invest, or retire comfortably.

The Great Malaysian Love Affair With Cars

Let’s be honest.

Malaysians love cars.

Some people change cars more often than they change mobile phones.

The moment a bonus comes in, somebody is already browsing car websites and calculating monthly instalments.

“Only RM1,500 a month.”

“Only RM2,000 a month.”

The word “only” has probably destroyed more wealth than inflation.

Most buyers focus on three things:

✅ Monthly instalment

✅ Down payment

✅ Car colour

Very few ask:

❌ How much interest am I really paying?

❌ What happens if I settle the loan early?

❌ Is the advertised interest rate actually the real interest rate?

Unfortunately, under the old system, the answer was often not very transparent.

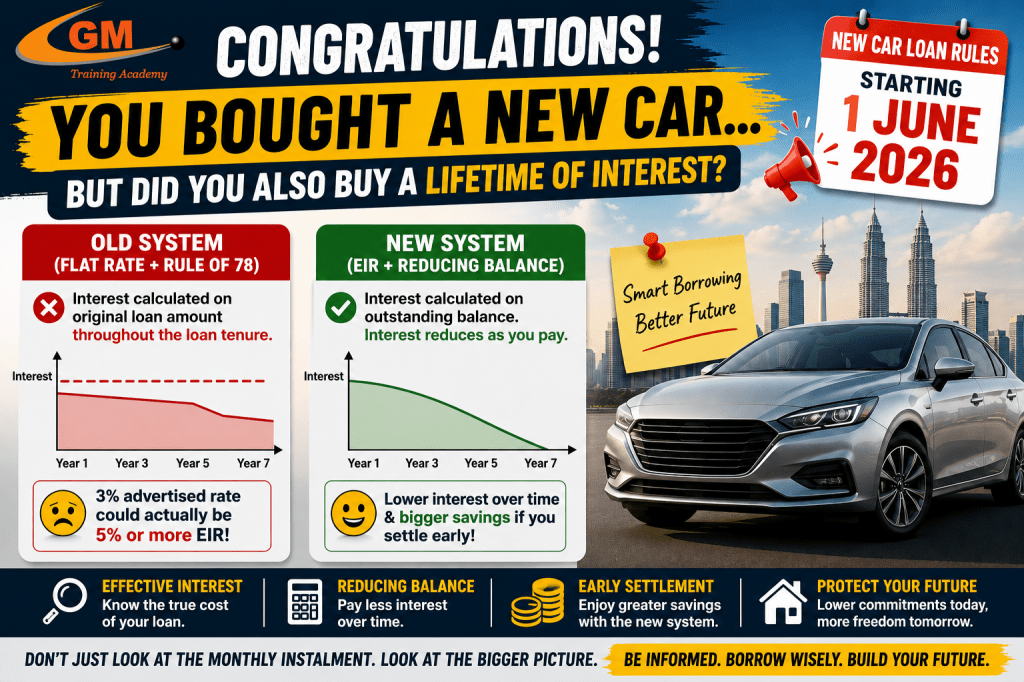

The Problem With the Old Car Loan System

For decades, Malaysian hire purchase loans used something called the flat rate system together with the infamous Rule of 78.

Sounds like something from a mathematics textbook nobody wanted to read.

Here’s what it actually meant.

Imagine you borrow RM60,000 to buy a car.

Under the old system, interest was calculated based on the original RM60,000 throughout the entire loan period.

Even after years of making payments and reducing your debt, the interest calculation still pretended you owed the full amount.

It’s like renting a hotel room for ten nights and still being charged for all ten nights even after checking out on Day 3.

Makes no sense, right?

Yet that was effectively how many car loans worked.

The Rule of 78: The Rule That Nobody Asked For

Then comes the famous Rule of 78.

This method front-loads interest payments.

In simple English:

The bank takes most of the interest first.

You reduce the principal later.

That means during the early years of your loan, a large portion of your monthly instalment goes towards paying interest rather than reducing your actual debt.

This creates a frustrating situation.

After faithfully paying your instalments for several years, you decide:

“I want to settle my loan early and save money.”

You call the bank.

Then you receive the settlement figure.

And suddenly you wonder whether the bank accidentally sent you somebody else’s loan balance.

The amount still looks surprisingly high.

Why?

Because under the old structure, you already paid a significant portion of the interest upfront.

The “3%” Loan That Wasn’t Really 3%

This is where things become interesting.

Research highlighted that a car loan advertised at a 3% flat rate could actually be equivalent to approximately 5.5% Effective Interest Rate (EIR).

In other words:

The number you saw wasn’t necessarily the true cost of borrowing.

Imagine walking into a restaurant and ordering a RM10 nasi lemak.

After taxes, service charge, packaging fee, convenience fee, and mystery fee, the bill becomes RM18.

Technically, nobody lied.

But the full picture wasn’t exactly obvious either.

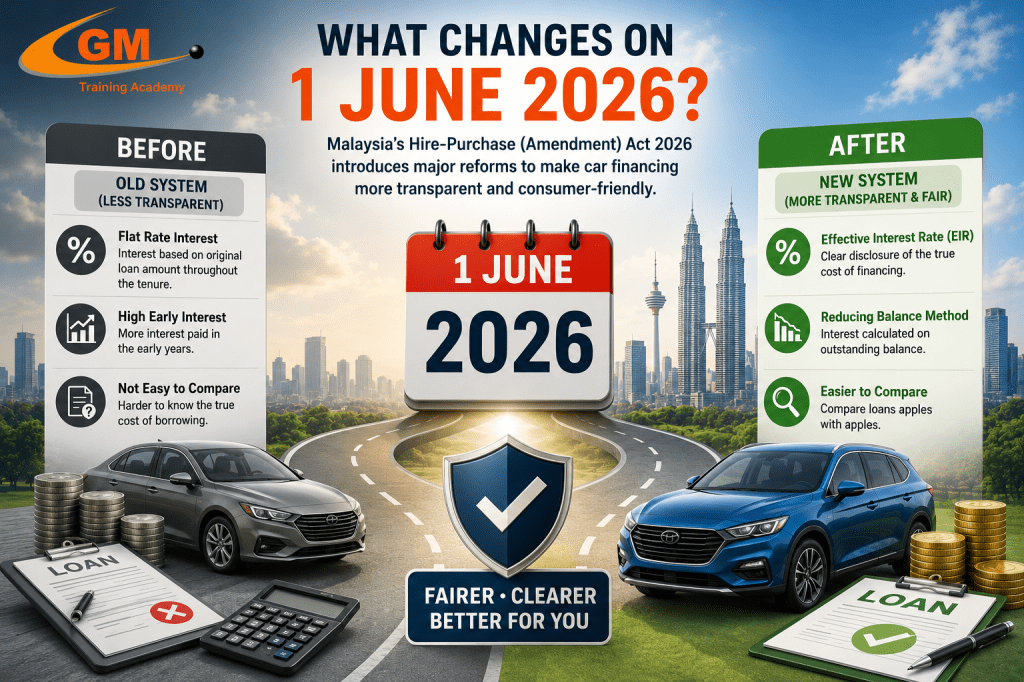

What Changes On 1 June 2026?

Malaysia’s Hire-Purchase (Amendment) Act 2026 introduces major reforms to make car financing more transparent and consumer-friendly.

The two biggest changes are:

1. Effective Interest Rate (EIR)

Banks must disclose the Effective Interest Rate.

This shows the true cost of financing and allows consumers to compare loans more accurately.

Finally, borrowers can compare apples with apples instead of apples with durians.

2. Reducing Balance Method

Interest will now be calculated based on the outstanding loan balance.

As your debt decreases, your interest charges also decrease.

This is similar to how housing loans have long been calculated.

And frankly, many people are wondering why car loans didn’t work this way years ago.

Why This Matters More Than Most People Think

Many Malaysians view a car as transportation.

But financially speaking, a car is often the second-largest purchase after a house.

A small difference in financing costs can mean thousands of ringgit over the life of a loan.

More importantly, excessive car commitments can affect:

- Home loan eligibility

- Debt service ratio (DSR)

- Monthly cash flow

- Investment capacity

- Retirement savings

I’ve met people driving luxury vehicles while claiming they cannot afford a property deposit.

Sometimes the issue isn’t income.

It’s debt allocation.

A RM2,500 monthly car commitment can dramatically reduce your borrowing power for property investment.

The Biggest Winner: People Who Settle Early

This is perhaps the most consumer-friendly improvement.

Under the new reducing balance system, borrowers who settle early can enjoy significantly greater savings because future interest charges reduce together with the remaining principal.

In short:

Being financially responsible finally gets rewarded.

What a revolutionary concept.

Existing Borrowers Are Not Completely Left Out

If you already have an existing car loan, don’t rush to the showroom and buy another vehicle just because the rules changed.

Existing agreements generally remain under their original structure. However, banks have announced a goodwill discount initiative for eligible borrowers who choose to settle their loans early after the new framework begins.

If you have been considering early settlement, it may be worth contacting your bank and asking for the updated settlement figure after June 2026.

You might be pleasantly surprised.

The Real Lesson Isn’t About Car Loans

This story isn’t really about car loans.

It’s about financial literacy.

Too many people buy based on monthly instalments.

We should instead focus on:

- Total repayment amount

- Effective borrowing cost

- Opportunity cost

- Impact on long-term wealth

Before signing any loan agreement, ask yourself:

“Will this purchase move me closer to financial freedom or further away from it?”

The answer might change your decision.

Final Thoughts

The new car loan rules are a positive step for Malaysian consumers.

Greater transparency.

Fairer interest calculations.

Better early settlement benefits.

All of these should help borrowers make smarter financial decisions.

But remember:

The cheapest car loan is not necessarily the best financial move.

And the best financial move is not always the newest car.

Sometimes the smartest investment is not what sits in your driveway.

It’s what sits in your bank account, your investment portfolio, or your property portfolio.

Because while a car helps you reach your destination…

Financial freedom helps you choose where you want to go.

From the Desk of

Miichael Yeoh

Disclaimer: This reflects the author’s personal views based on market experience and current observations. It is not financial advice. Smart investors do their own research before making any move.

Leave a comment